Taxes on the Brain

BY: ETHAN LOHR, CFP® — March 2026

It’s that time of year when taxes are top of mind. Forms have arrived in the mail, calls and emails are being exchanged with the accountant, and many households are taking their annual look at what they paid and what might be different next year.

While tax season naturally focuses our attention on last year’s numbers, it can also be a helpful moment to step back and think more broadly about how taxes fit into the bigger financial picture. The most impactful tax decisions are rarely made at filing time—they’re often the result of planning that happens months or even years in advance.

With that in mind, I wanted to share a few ideas that may serve as thought-provokers. Some of them may even feel a bit counter to how taxes are commonly approached. But as we’ve seen in working with many households over the years, sometimes the most effective tax strategies involve thinking about taxes a little differently than we might at first expect.

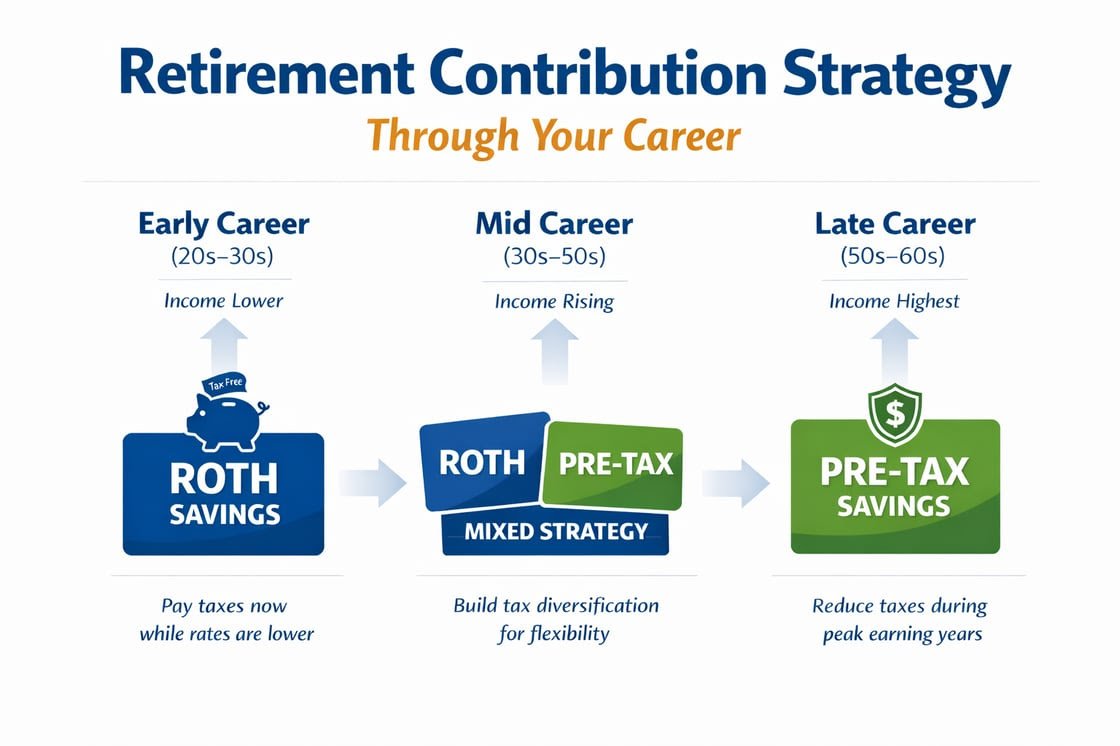

Tax Location for Retirement Savings

Our first idea is a simple way to think about retirement contributions. While this one isn’t necessarily counterintuitive, it provides a helpful framework for savers across the career spectrum when deciding how they should save.

For the sake of simplicity, assume today’s tax brackets remain constant in the future—something that may or may not actually happen. But the core idea is straightforward: pay taxes when you save for retirement while you’re in lower brackets, and reduce taxes when you save during higher-earning years.

In practical terms, that means younger savers often benefit from prioritizing Roth contributions, paying taxes today while their income—and tax rate—may still be relatively low. As earnings rise later in a career, shifting more toward pre-tax contributions can help reduce taxes during peak earning years.

This approach also helps avoid a couple of common pitfalls. A young saver shouldn’t default to pre-tax contributions simply because they want a slightly larger paycheck or tax refund today. Likewise, someone nearing the end of their career shouldn’t shift heavily toward Roth contributions simply because they wish they had started a Roth sooner.

Instead, the decision should be guided by a simple question: When does it make the most sense to pay the taxes?

Retirement Income First, Tax Optimization Second

Our second tax planning idea centers around income in retirement.

It’s common to hear discussions about how retirees should manage taxes once they stop working. Topics like mitigating IRMAA surcharges, managing Medicare premiums, and timing Roth conversions are often part of the conversation.

While these are all worthwhile planning considerations, what we often see is retirees attempting to plan for everything—ultimately leaving them without a clear plan at all.

Are there ways to optimize taxes around different brackets and thresholds? Absolutely. But step one is establishing an income strategy that is both enjoyable and sustainable.

Just as you wouldn’t question a pay raise at work simply because it means paying more taxes, the same thinking shouldn’t suddenly take over in retirement. Taxes are a factor, but they shouldn’t dictate every decision.

Concerns about tax thresholds and planning opportunities should take a back seat to something more important: creating the lifestyle you’ve envisioned for retirement. Once that income framework is in place, tax strategies can then be layered in thoughtfully around it.

Giving, Giving, Never Stopping

I was reading Paddington Bear to my oldest daughter recently, and the phrase “hurrying, hurrying, never stopping” appears at both the beginning and end of the story. As I began writing this section, that line popped into my head.

What if generosity worked the same way?

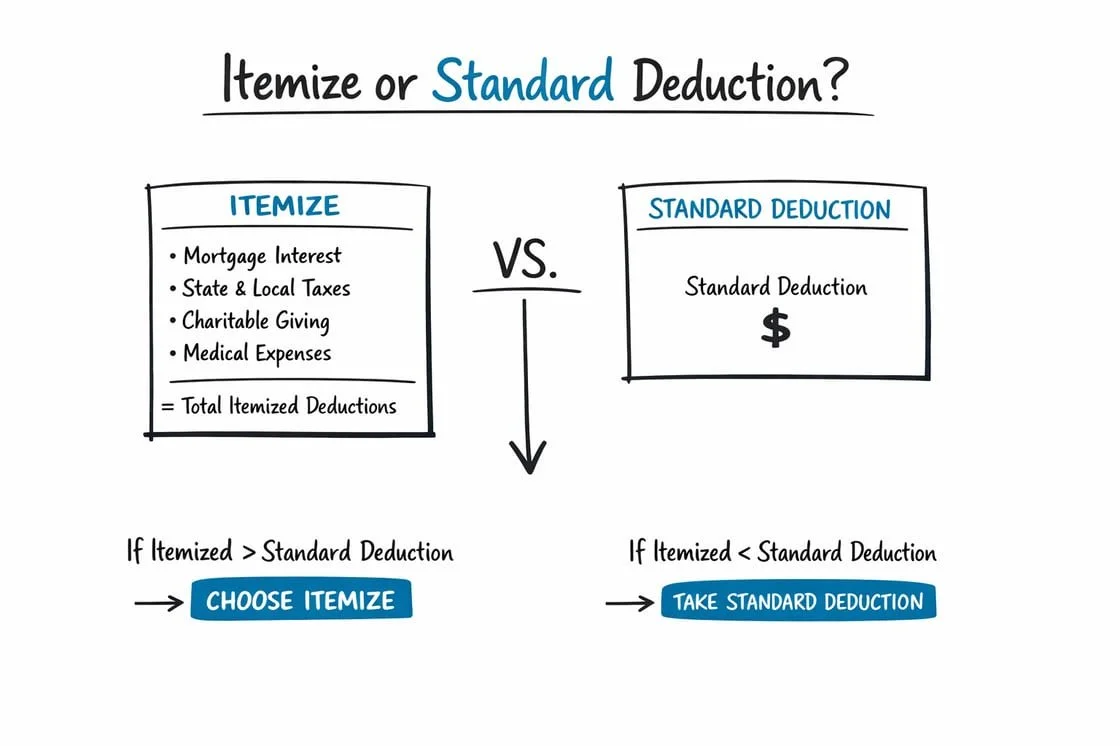

It’s often discussed how the current tax code doesn’t provide as strong of a tax incentive for charitable giving as it once did, largely because of the higher standard deduction thresholds for both single filers and married couples. Here’s the calculus:

While it may be true that the tax benefit isn’t as great as it once was, the practice and purpose of giving remains one of those good, timeless habits.

There are certainly ways to structure charitable giving so that it has a meaningful impact on your taxes in a particular year. Strategies such as donor-advised funds (DAFs), for example, allow individuals to give larger amounts in a single year to capture the tax benefit while distributing those gifts to charities over time.

But what I’m referring to here is something a little different.

It’s the practice of giving regularly—weekly or monthly—just like many of the other rhythms in our lives. Much like when our paycheck arrives, or when someone else’s doesn’t. Or when we pay our utility bills and the charities we support must pay theirs.

Giving in this way moves beyond tax strategy and wealth optimization and becomes something entirely different—a shift in focus away from ourselves and toward others. That’s a benefit in its own right.

In Closing

So, here are a few ideas worth holding onto ranging from practical planning all the way down to ethos.

A special thank you to all of the tax preparers working long hours right now. As we all come up for air after completing taxes for the year, it’s a good opportunity to step back and consider how we can be both smarter and more thoughtful with the abundance that we have!

Enjoy this type of content?

Join our newsletter below and get it delivered right to your inbox.